Business Valuation in Morocco requires more than applying generic DCF formulas or copying EBITDA multiples from international markets. It demands a structured understanding of Morocco’s tax regime, sector dynamics, capital market depth, private company risk premiums, and regulatory framework.

For investors, founders, and boards, valuation is not a theoretical exercise — it directly impacts negotiation power, transaction structuring, tax exposure, and long-term strategic positioning.

This guide explains how valuation is actually performed in Morocco, what drives premiums or discounts, and how sophisticated buyers assess risk.

Table of Contents

Executive Overview: The Moroccan Valuation Environment

Morocco’s corporate ecosystem sits between emerging-market volatility and structured institutional reform. The country benefits from:

- A stable monetary framework (managed exchange regime)

- Controlled inflation (historically around 2–3%)

- Progressive corporate tax reform (20%–35%)

- Growing foreign direct investment

- Strategic positioning between Europe and Africa

However, the M&A market remains relatively small and less transparent compared to GCC hubs. Publicly disclosed transaction data is limited. This lack of transparency increases reliance on professional judgment, cross-border comparables, and structured financial normalization.

Recent publicly disclosed M&A activity in Morocco has hovered around MAD 2 billion annually, reflecting a developing but still selective transaction environment.

In this context, valuation must be rigorous, conservative, and scenario-driven.

Core Valuation Methods Applied in Morocco

In practice, professional advisors triangulate at least two approaches to establish a credible valuation range.

1. Discounted Cash Flow (DCF)

The DCF method projects future free cash flows and discounts them using a weighted average cost of capital (WACC).

In Morocco:

- WACC typically ranges between 10% and 15%.

- Terminal growth assumptions usually fall between 2% and 4%.

- Corporate tax (20%–35%) materially affects after-tax cash flow.

DCF is dominant for:

- Established profitable companies

- Export-driven industrial groups

- Infrastructure and utility assets

- Companies with reliable forward projections

Its strength lies in forward-looking analysis. Its weakness lies in sensitivity to assumptions — especially in emerging market contexts.

2. Market Multiples (Comparable Analysis) in Morocco

Market-based valuation derives value from multiples such as:

- EV/EBITDA

- EV/Revenue

- P/E

Due to limited local disclosure, advisors often combine:

- Moroccan listed companies

- Regional MENA comparables

- Selected European benchmarks (adjusted for country risk)

Private companies generally trade at a discount to listed multiples.

Typical private discount range: 20%–50%

Drivers include:

- Illiquidity

- Governance structure

- Disclosure quality

- Scale limitations

3. Asset-Based Approach

Used when:

- The company is asset-heavy

- Earnings are unstable

- Real estate drives value

- The business is distressed

Assets are revalued to fair market value.

Liabilities are adjusted to realistic settlement cost.

Common in:

- Real estate holding companies

- Industrial land-intensive firms

- Companies owning strategic property in Casablanca or Tangier

This method often acts as a valuation floor.

4. Profit Capitalization Method in Morocco

Frequently used in SMEs where:

- Financial reporting is inconsistent

- Informal transactions exist

- Projections are unreliable

Normalized profit is capitalized using a sector-adjusted rate.

While simpler, this method requires strong financial reconstruction before application.

Comparison of Valuation Approaches in Morocco

| Method | Best Used For | Strength | Limitation |

|---|---|---|---|

| DCF | Profitable growth firms | Forward-looking | Sensitive to assumptions |

| Market Multiples | Active sectors with comps | Market-aligned | Limited local data |

| Asset-Based | Property-heavy firms | Conservative floor | Ignores future upside |

| Profit Method | SMEs | Simple | Less precise |

In most transactions, DCF + Multiples form the primary valuation range, cross-checked against asset value.

Tax and Regulatory Factors That Directly Impact Valuation in Morocco

Corporate Tax Reform in Morocco

Morocco is implementing a progressive corporate tax structure:

- Around 20% for companies below MAD 100 million taxable profit

- Up to approximately 35% above that threshold

This reform materially changes:

- After-tax free cash flow

- Dividend capacity

- Equity valuation

Ignoring tax structure leads to overstated valuation conclusions.

Official tax framework references are available via the Moroccan Ministry of Economy and Finance.

Dividend Withholding Tax in Morocco

Changes in dividend taxation between 2023–2026 impact:

- Net investor return

- Dividend discount models

- Transaction structuring (asset vs share deal)

Investors often model valuation differently depending on expected distribution policy.

Special Regimes in Morocco

Companies operating under:

- Industrial Acceleration Zones

- Casablanca Finance City status

- Export-driven incentives

May benefit from preferential rates.

However, valuation premiums must assess sustainability and compliance risk. Incentives subject to regulatory review should not be capitalized blindly.

Sector EBITDA Multiples Snapshot (Public Benchmarks) in Morocco

Recent public company benchmarks illustrate sector variation:

| Sector | EV/EBITDA Range | Commentary |

|---|---|---|

| Banking | 6x–10x | Stable but regulated |

| Telecom | 6x–8x | Mature growth |

| Utilities | 10x–20x | Infrastructure premium |

| Retail | 8x–10x | Margin-sensitive |

| Fintech | 12x–18x | Growth premium |

| SaaS | ARR-based | 4x–10x ARR typical |

Technology and export-oriented manufacturing command higher multiples due to growth and scalability.

Traditional domestic services trade lower due to slower expansion and informality exposure.

How Investors Adjust Value in Morocco

Sophisticated buyers apply adjustments beyond textbook formulas.

1. Informality Discount

In smaller companies:

- Off-book sales

- Weak documentation

- Related-party transactions

Lead to valuation reductions or require financial reconstruction.

2. Customer Concentration Risk

If top client represents >30% revenue, buyers apply risk premium.

3. Leverage and Debt Structure

High debt reduces equity value significantly.

Enterprise value must be converted properly:

Enterprise Value

– Net Debt

= Equity Value

4. Country Risk Premium

Morocco benefits from macro stability, yet emerging-market risk remains priced into WACC.

Valuation by Situation

Valuation purpose changes methodology emphasis.

M&A Transaction

Focus on control premium and synergies.

Minority Buyout

Liquidity discount applied.

Litigation / Shareholder Dispute

Court-compliant independent report required.

Tax Planning

Conservative approach to withstand authority review.

Fundraising

Growth premium emphasized.

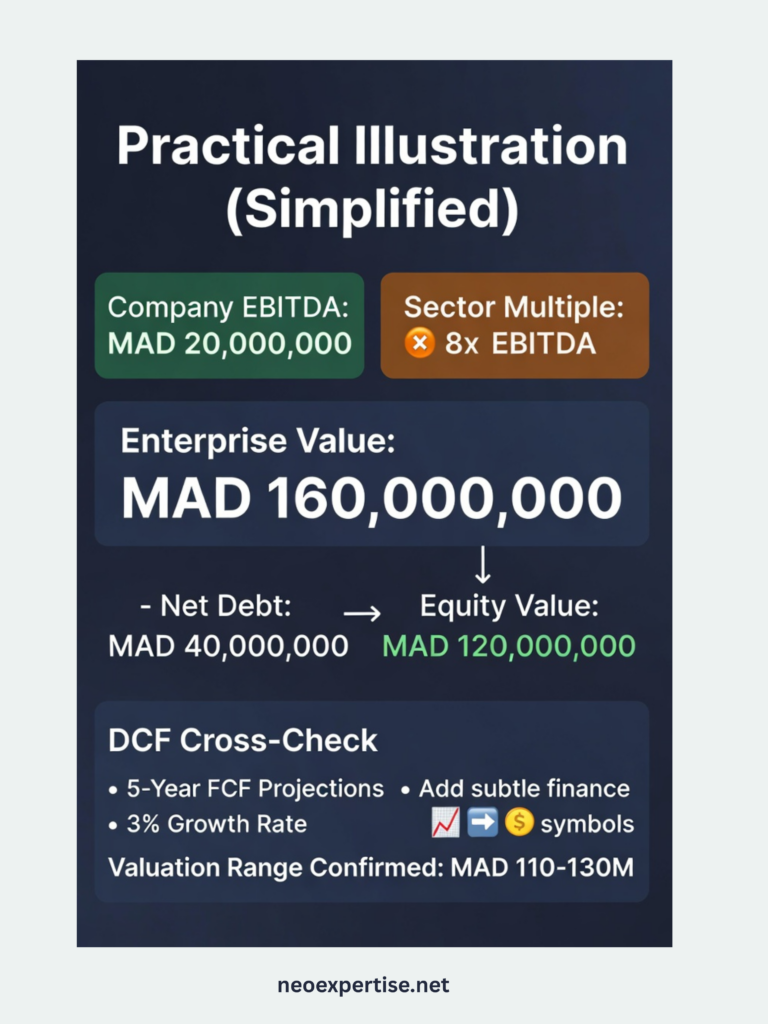

Practical Illustration (Simplified)

Company EBITDA: MAD 20 million

Sector multiple: 8xEnterprise Value: MAD 160 million

Net Debt: MAD 40 million

Equity Value: MAD 120 million

DCF cross-check would test whether projected free cash flows justify similar range.

Frequently Asked Questions

How do you value a company in Morocco?

Using DCF and market multiples.

Is DCF commonly used in Morocco?

Yes, for profitable firms.

What is a typical EBITDA multiple?

Usually 6x–15x by sector.

Are private companies discounted?

Yes, 20–50% typical.

Who performs business valuation?

Certified valuation advisors.

Conclusion

Business Valuation in Morocco requires combining international valuation standards with local tax structure, regulatory considerations, sector benchmarks, and transaction realities.

Generic formulas are insufficient. Investors and shareholders must analyze:

- Tax regime impact

- Sector growth profile

- Private company risk discount

- Capital structure

- Regulatory environment

A rigorous, independent valuation process provides negotiation clarity, tax defensibility, and strategic insight.

At Neo Expertise, we support shareholders, investors, and management teams through structured, independent valuation mandates. Our approach combines financial modeling, sector benchmarking, tax impact analysis, and transaction context to deliver defensible valuation ranges aligned with Moroccan regulatory standards.

Whether the objective is a transaction, minority buyout, restructuring, litigation support, or capital raising, Neo Expertise provides valuation reports designed to withstand investor scrutiny and regulatory review.

If you are considering a transaction or need an independent valuation assessment, our advisory team can guide you through a structured and confidential process tailored to your sector and strategic objectives.

Brahim Rami | Member of institute of chartered accountants in Morocco

He is a CPA and tax advisor, founder of NeoExpertise.net, a Legal and Tax firm helping foreign companies with business setup, due diligence, payroll, and tax compliance in Morocco and Africa.